How Investors Are Handling Covid’s Third Act Twist

Posted on — Leave a commentThe biggest surprises always come in the third act. Covid is no exception.

The Delta variant continues to cause a surge of infections and deaths as 30% of those in the US still remain unvaccinated. As Dr. Anthony Fauci put it, “things are going to get worse.”

As the seven-day average of new daily cases rises businesses and investors are tempering their outlook. Previously the U.S. was experiencing approximately 10,000 cases a day. By early August that figure grew to about 84,000 and continue to increase. Recent estimates suggests that the number could get as high as 200,000 cases a day.

Investors and businesses are already taking action.

How do we know? Money-markets funds and banks are seeking ways to earn a safe and predictable return on their excess cash. They are doing so with a transaction called a reverse repurchase agreements, or “repos.”

In this kind of transaction, the lender purchases an asset like equipment or shares from the seller with an agreement to sell those same assets back to the seller at a set future date for a higher price. Today, money-market funds and banks are engaging in repos to the tune of $1 trillion in cash. This amount is the highest on record since the Federal Reserve allowed these kinds of transactions in 2013. The main reason for the influx of cash is likely the central bank’s decision to inch up their interest rate from 0% to 0.05%.

What is more concerning is the fact that this increase in repos might suggest that more institutions are in need of cash to fund short-term operations.

Meanwhile Moody’s Analytics has designed a “Back-to-Normal Index” intended to track the latest economic data. These metrics include things like the number of people flying, restaurant bookings and initial claims for unemployment benefits. This figure is beginning to look troubling for certain areas of the US, especially the south. Today, the index has fallen from it’s high reached in late June of this year.

Additional nation-wide lockdowns remain unlikely, and many experts believe the increase of hospitalizations will encourage at least some vaccine skeptics to get the shot. Despite this, the expectation for a booming summer and phenomenal second half to 2021 for investors is beginning to dim.

Proactive investors are taking this opportunity to read the road and make their smart moves before it is too late. For many this means keeping a significant amount of dry powder so that they can act when opportunities, like dropping asset prices, are presented. For others it means exploring the possibility of “safe haven” assets like gold that tend to benefit in climates of uncertainty and falling economic and business confidence.

It is too soon to know the extent of Delta’s economic impact. What we do know is that the situation is escalating and creating a picture much different than what most forecasted even one or two months ago. Medical professionals have also warned of the possibility that further variants can develop as we move into the winter months. The covid pandemic will end, but investors need to be prepared for a longer third act.

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.

The Intriguing Numismatic Theory Behind This Coin

Posted on — 1 CommentAmericans had mixed feelings about the $3 gold piece. In the late 1880’s the $3 Indian Princess Head was worth well over a day’s pay.

well over a day’s pay.

What’s more – it carried an odd number.

It turns out that very few people wanted to use coin which did not fit into the already accepted decimal calculations. Even though it was not heavily used in circulation – the $3 gold piece instantly captured the attention of coin collectors.

Numismatists began avidly seeking out and saving the intriguing $3 Indian Princess gold coin as early as 1879.

So why did the U.S. Mint decide to produce a $3 gold coin – especially since they already had a gold quarter eagle worth $2.50?

The surprising theory behind the origin of this coin is an unlikely culprit: a U.S. postage stamp. When this coin was minted a U.S. postage stamp cost 3 cents.

Numismatists believed that the sole purpose for creating the $3 coin was to create a convenient way for businesses to purchase 100 stamps in a single transaction.

Every U.S. coin denomination has a number of rarities. Yet, the $3 Indian Princess Head, minted from 1854-1889, is packed with so many low-mintage dates that the entire series is considered rare.

In 1880, for example, only 1,000 were minted. In 1881 only 500 were minted. And in 1882, only 1,500 were minted. Plus, many were lost to the melting pot in the 1930’s, reducing the number of survivors available today.

Many consider the $3 Indian Princess the most beautiful gold coin struck in the 19th century. See the rich and warm patina that comes with a 141 year old masterpiece here.

Designed by the U.S. Mint’s chief engraver, James B. Longacre, the $3 gold coin was the first time he had been given the freedom to create a design of his own. Longacre wrote that, previous to the $3 gold coin, he had been directed to adapt Roman or Greek features into U.S. coins. For the $3 gold coin, Longacre was determined to create something uniquely American.

“From the copper shores of Lake Superior to the silver mountains of Potosi, from the Ojibwa to the Araucanian, the feathered tiara is a characteristic of the primitiveness of our hemisphere as the turban is of the Asiatic,” Longacre wrote.

He was inspired to feature an “Indian Princess” on the obverse of this stunning coin. A lustrous orange-gold color, the coin shows a gorgeous Indian Princess adorned with a feathered headdress, with the words UNITED STATES OF AMERICA encircling her. On the reverse, the date and denomination is surrounded by an agricultural wreath celebrating corn, tobacco, cotton, and wheat.

Rare Coin Market Update

This summer we are seeing huge numismatic demand and extremely low inventory levels, which is contributing to rising prices.

In June 2021, the Rare Coin Values Index hit a new all-time record high of 434.28. (The Rare Coin Value Index is based on the combined percent change in retail prices for 87 rare United States coins and is updated monthly.)

Numismatic rarities that come onto the market can sell in a matter of days due to the limited supply and strong investor interest. Long-time numismatic investors are holding and expanding their collections when they can.

Investors are seeking opportunities to diversify their portfolios and protect and grow their wealth through tangible assets like rare coins – that are a non-correlated asset to the stock market. If there is a coin that you seek, call us today. We are often able to source even hard-to-find coins due to our deep connections inside the numismatic community.

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.

Don’t Count on the Fed to Protect Your Wealth

Posted on — Leave a commentThe Federal Reserve met today and delivered once again – a whole bunch of nothing.

The Fed did not raise interest rates from zero percent and indicated it would keep on buying $120 billion in U.S. government bonds each month. The Fed said the U.S. economy continues to strengthen and that the recent burst of inflation is transitory. Really?

After the Fed meeting, gold traded $11.00 higher at $1809.70 an ounce.

In fact, many economists are beginning to cite concerns about the recent slowdown in economic growth and rising inflation – often called “stagflation.” Despite the Fed’s upbeat outlook, recent data revealed that the U.S. economy actually cooled in June, with the Chicago Fed National Activity Index falling sharply.

Is the Fed right to hold its course – keeping its easy money policies in place? Many aren’t so sure.

News reports indicate that divisions are forming within the Federal Reserve and some regional bank presidents believe the Fed should start tapering its bond purchases.

You may remember, the Fed began buying $120 billion in bonds each month last summer in an attempt to stabilize the financial system and spur demand after the Covid crisis hit. Why should we care? The Fed bond-buying artificially depresses interest rates and essentially monetizing our debt (when Congress passes spending bills and the Fed buys our bonds to pay that debt).

Indeed, the house of cards gets more precarious every month – which highlights the value of holding assets like gold in your portfolio to preserve and protect your wealth in non-dollar assets.

What’s more – inflation is running really hot! In June, the consumer prices index soared 5.4% over the past year – and the Fed keeps its easy money policies in place. Fed Chairman Jerome Powell admitted today that “inflation is running well above our 2% objective.” Yet, they keep interest rates at zero percent. Never before in history have we seen a Federal Reserve so lackadaisical about inflation.

This is yet another reason investors might want to consider increasing their allocation to gold during these curious times. History shows that gold increases in value along with other commodities, like real estate, during inflationary periods. Gold is real money that can’t be manipulated by the Federal Reserve’s printing presses.

How high will inflation have to run before the Fed acts – and then will it be too late – without inflicting major damage to the economy? Don’t wait to find out. Your dollars buy even you more gold right now.

Gold is a bargain at today’s prices – well below its record all-time high above $2,063 an ounce. “Gold is relatively cheap so when you’re trying to think about that positioning, gold is definitely one that still has catch-up potential,” TD Securities’ Richard Kelly recently told CNBC.

As the Federal Reserve continues to ignore hard evidence of rising inflation and is a willing participant in the monetization of U.S. debt – gold will continue to climb in value in the future, while the government devalues the U.S. dollar via its money-printing strategy.

While you can’t count on the Fed to protect your wealth, you can act now with an increased allocation to tangible assets like gold and silver. Trading your dollars for gold is a smart money move.

In gold we trust.

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.

Gold and Climate Change

Posted on — Leave a commentThe issue of climate change has long been politicized and the effects will be experienced by those on both sides of the political spectrum. In response, countries like China have committed to becoming carbon neutral by 2060. The U.S. has  targeted a goal of attaining 100% carbon pollution-free electricity by 2035. These dramatic measures have left some gold investors questioning how the energy intensive nature of mining will keep pace with a changing world. A report from the World Gold Council offers some answers.

targeted a goal of attaining 100% carbon pollution-free electricity by 2035. These dramatic measures have left some gold investors questioning how the energy intensive nature of mining will keep pace with a changing world. A report from the World Gold Council offers some answers.

A key finding of their research shows that the emissions intensity of gold production is forecast to fall 35% by 2030. Accomplishing this decrease will require a move from conventional energy sources like diesel, coal, and heavy fuel oil to renewable resources. Those leading the charge on decarbonization will keep a close eye on mining operations given that they consume an estimated 11% of global energy.

Despite the commitment to reducing emissions there are considerable challenges ahead, namely the increasing scarcity of gold deposits. With every passing year it becomes more difficult to source new mines. As a result, there is an increased geographic dispersal of projects. This characteristic of mining today means that more projects are in remote areas leading to higher energy consumption as more resources are needed to yield a profitable output from new mines. This dynamic is a major reason why “the total energy consumption of the sector has risen approximately 23% over the last 5 years,” according to the World Gold Council.

Despite this rise there is reason for optimism. The same report found that of the 158 mines examined 104 were tied into the grid and that grid-sourced electricity represented more than half of the total annual power consumption. This has major implications for decarbonization given that those who do not have grid connectivity often resort to carbon-intensive resources to maintain their operations.

Meanwhile, technology is beginning to afford more creative options for sourcing gold without the need for a single drill. The world is awash in electronics that have gold components. It is estimated that only 15% of the gold within the tons of devices discarded every day is recycled. In fact, each year the world manufactures electronics that in total are home to $21 billion worth of gold and silver according to the United Nations University, a global think tank. Recent developments have led to a process in which discarded electronics can be subjected to an acid bath which leaches out the metals within and allows scientists to isolate approximately 94% of the gold dissolved from the circuit boards. It is likely that these methods of recycling gold will become more popular and more sophisticated as traditional mining faces challenges in totally moving away from carbon emissions.

Yielding gold in a carbon-free setting will require considerable effort in which numerous measures add up to meaningful change. The combination of a greater reliance on renewable energy, grid connectivity, and gold recycling can create a measurable difference.

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.

1989 Japanese Nikkei Stock Market Crash: Learning from History

Posted on — 1 CommentOn Monday, the Dow Jones Industrial Average plunged 1.72%, marking its biggest one-day drop since October. While the market bounced back Tuesday, stock market breadth has been declining, which is a warning signal that a correction may be near.

Wall Street defines a stock market “pullback” as a retreat of 5-10% and is a short-term dip. A “correction” phase is more serious and is defined as a 10-20% retreat from the recent high and can last several months.

Bear markets in stocks occur after a 20% decline or more that lasts two months or more.

One of the difficulties is that no one really knows if a pullback will turn into a correction, and if that correction will turn into a bear market. Panic selling, financial news stories and even social media can intensify investor fear, which in turn creates fresh stock selling and downside momentum.

Is your portfolio ready for a stock market correction, or something even more severe?

Consider this:

Bear markets tend to last on average approximately 16 months – or well over a year. During the 2007-2009 bear market, the S&P 500 crashed 57%.

Yet here in the U.S., Wall Street’s worst bear market occurred after the Great Depression. The Dow Jones Industrial Average took 25 years to recover to its previous peak.

In Japan, the Nikkei stock index still hasn’t fully recovered from the infamous stock market crash in 1991 – and it’s now thirty years later!

Japan’s Nikkei stock index hit its all-time high at 38,915 in December 1989 during an asset-inflated economic boom there (sound familiar?). The Japanese stock market crashed after the Japanese Central Bank was forced to tighten monetary policy, and it still has not fully recovered.

From 1991 until 2009, the Nikkei stock index etched a dramatic 81% decline.

Have you heard George Santayana’s quote?

“Those who cannot remember the past are condemned to repeat it.”

According to Santayana’s philosophy, history repeats.

More recently, the U.S. stock market has recovered from bear markets in a matter of years. But, history shows it can take decades to get back to breakeven. Case in point – the U.S. stock market after the Great Depression and the Japanese Nikkei stock market crash.

In the U.S. we are currently in the midst of an equity asset boom – driven in large part by experimental Federal Reserve monetary policy with zero percent interest rates. The Federal Reserve has never before expanded the money supply like it has during the Covid crisis, unleashing the potential for inflation and possibly even severe inflation.

The recent jittery behavior in the stock market, combined with technical signals like declining market breadth (fewer and fewer stocks are making new highs), flashes a big red warning signal that volatility may lie ahead.

How would you fare if the stock market crashed 60% or 80% and then took decades to get back to breakeven? It happened before here in the U.S. and more recently in Japan.

Have you considered increasing your allocation to tangible assets like rare coins and gold and silver bullion? Both these asset classes historically delivered double-digit gains during inflationary periods and big stock market declines.

The canary in the coal mine is singing now. Are you listening?

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.

Why Do Central Banks Intend to Increase Gold Reserves in the Next 12 Months?

Posted on — Leave a commentA 2021 Central Bank Gold Reserves survey concluded that 21% of central banks plan to increase their gold reserves over the next 12 months. The question is why.

The one-word answer: uncertainty.

The same body of research found that 84% of the respondents cited uncertainty arising from the post-COVID recovery as a major influence over their decision to bolster their gold holdings. Interestingly, 52% of the survey participants indicated that they think global central banks will increase their gold holdings in the coming year. The World Gold Council explains that these moves highlight “the importance of maintaining liquid, uncorrelated assets in a reserve portfolio.”

Put simply, central banks are purchasing more gold today due to its performance during periods of crisis. The events of the last 15 months have made risk a central focus for businesses, governments, and institutions planning for the future. Central banks have made it a strategy to build their gold reserves not only to safeguarding against uncertainty, they also hold gold due to its lack of default risk, its ability to store value over the long-term, and its freedom from political risk.

The increase of gold purchases in central banks across the globe are also likely in response to fears of rising inflation. Previous research from the World Gold Council shows that “gold had an annual average return of 15% in years when the US Consumer Price Index (CPI) was higher than 3%.” Additionally, as international trade slowly resumes more countries are equipped with the capital to boost their gold reserves.

Gold has a heightened relevance in a world where uncertainty looms large. When gold is included as part of a diversified portfolio it serves as an uncorrelated asset and can provide additional protection as the value of the US dollar falls. This characteristic of gold has a strong influence over central bank stakeholders. Consider that the survey found that half of the responders believe the dollar will drop in value in the near-term.

However, the uncertainty that worries central banks is not just about the US. While, nearly 70% of those 18 and older in the US have received at least one dose of the vaccine leading to a strengthening economic recovery this return to normalcy is not evident across the globe. Many countries continue to struggle. Some of the most devastated areas are suffering their worst case count since the pandemic began. This environment has major implications for central banks everywhere including the US because gold is an asset used in international trade and has value that is universally understood.

Simply put, while the economic outlook improves in the US, the situation remains dire elsewhere. This is the reason central bank gold holdings are set to grow over the next 12 months. These anticipated purchases may bolster the value of gold due to both supply and demand dynamics and a heightened awareness of the safeguarding effect gold has on a diversified portfolio.

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.

Barber Left the Motto Off This Silver Coin

Posted on — Leave a commentU.S. Bureau of the Mint Chief Engraver Charles E. Barber designed the famed Barber coinage which includes a dime, quarter and half dollar. And, Barber dimes were struck from 1892 through 1916.

This beautiful silver coin features Lady Liberty facing right on the obverse. UNITED STATES OF AMERICA encircles her head. The date is found below Lady Liberty’s bust. The dime’s reverse reveals a delicate and ornate Laurel wreath wrapped around the coin’s denomination: ONE DIME in the center.

There was no room for the motto IN GOD WE TRUST on the Barber dime. So, Barber left it off. Barber did find room to include the motto on the quarter and half dollar designs.

Another difference? One legendary numismatist wrote this about the Barber dime:

“It is not generally realized that the obverse design of the dime differs from that of the quarter and half dollar, in that the latter denominations have stars around the obverse periphery.”

In 1900, the U.S. minted over 17 million Barber dimes at the Philadelphia Mint. Only 600 proofs were struck. Survival estimates of all grades of 1900 Barber dimes are less than 1,000. See this delightful 1900 Barber dime proof, with a smattering of orange-apricot iridescence sparkling at the rims here.

The rarest of all Barber dimes is the 1894-S Barber dime. The San Francisco mint struck only 24 of these dimes. Great mystery surrounds the 1894-S Barber dime – and no one really knows why so few were coined. As one story goes, San Francisco Mint Superintendent John Daggett struck the dimes for his banker friends, giving three to each. Daggett also gave three to his daughter Hallie. Less than a dozen 1894-S Barber dimes are known to survive and one was sold in 2013 for over $2 million.

The year 1900: looking back in time

- In 1900, the U.S. Census estimated our country’s population at 70 million. (Today, the U.S. is home to 332 million people).

- In March 1900, Congress passed the Gold Standard Act, which established gold as the only standard for redeeming paper money.

- In April, 1900 Hawaii became an official U.S. territory.

- In October 1900, the Wright brothers started their manned glider test flights in Kitty Hawk, North Carolina.

- In 1900, Milton S. Hershey introduced the milk chocolate Hershey bar.

You can see this great Barber Dime here.

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.

The Seated Liberty Half Dime: An Enduring Symbol of Freedom

Posted on — Leave a commentThe U.S. half dime (originally the half disme), was minted in 1792 under the Coinage Act of the same year, and  is widely considered to be the first business strike coin issued by the United States Mint. However, there continues to be some debate as to whether the 1792 version was simply a pattern coin.

is widely considered to be the first business strike coin issued by the United States Mint. However, there continues to be some debate as to whether the 1792 version was simply a pattern coin.

Ostensibly, this means that the half dime was the first coin minted for the purposes of commerce rather than collecting. (The U.S. Mint, on the other hand, awards the 1793 Chain Cent this distinction). The name “half dime” was given because the coins were thinner than ordinary dimes and had a shorter diameter. The coin was minted for more than 80 years, and the Seated Liberty version marks the final version produced.

Seated Liberty half dimes were minted from 1837 to 1873. The design is considerably different from the original piece. The Seated Liberty depicts Liberty seated on a rock with a shield by her feet. She holds a pole in her right hand with a Phrygian cap on top. This detail is important because the Phrygian cap is a symbol of freedom and liberty. This association with the cap began around the time of the American Revolution and later during the French Revolution. The design of the cap resembles the Roman “pileus” worn by freed slaves in ancient Rome as a symbol of Libertas, the Roman goddess of liberty who wore the same cap. The imagery of the cap looms large in U.S. institutions, including the Army. Since 1778 the “War Office Seal” has depicted the motto “This We’ll Defend” directly above the Phrygian cap on an upturned sword.

The cap, however, was only part of the look of the coin. During the preliminary design stage, starting as early as 1835, artists relied on the silver dollar patterns of 1836. Throughout production, the U.S. minted the coin in Philadelphia, San Francisco and New Orleans. The total minting was more than 84 million coins.

Despite the massive number of half dimes minted, there have been a few rare finds. In the late 1970s, one collector caused ripples in the numismatic community when he claimed to own an 1870-S Half Dime. Official Mint records indicate that no half dimes were minted in San Francisco in 1870 which led to questions of authenticity. However, the coin was eventually deemed authentic and the coin sold at auction for $425,000. Today the same coin would have an estimated value of $1.5 million to $2 million.

To date, there is only one other known 1870-S half dime. This second piece earned $661,250 at auction in 2004. Other rare examples include uncirculated 1838-O versions minted in New Orleans.

The Seated Liberty Half Dime is a reminder of how much the symbolism of the U.S. and freedom changed between the year of the first half dime minting in 1792 and the final minting in 1873. The first design, known as the “Flowing Hair” half dime, included a simple profile of Liberty with long, wavy hair, in contrast to the vastly different Seated Liberty full of symbolism seen in the shield and Phrygian cap.

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.

Private Equity Firm Purchase Unleashes New Chapter in Rare Coin Market

Posted on — 1 CommentBreaking news. Just a few days ago, Blackstone, one of the world’s largest investment firms, acquired a majority stake in the Certified Collectibles Group (CCG). No small potatoes, this deal was valued at more than $500 million.

Who is CCG, you might ask? And, what does this mean for rare coin investors? Let us explain.

Founded in 1987, CCG provides independent certification on the value of collectibles such as rare coins, comic books, trading cards, sports cards, and more. The CCG companies include Numismatic Guaranty Corporation (NGC) – which is the world’s leading and largest third-party coin grading service.

Blackstone’s interest in buying a collectibles grading company reveals these investments are on the verge of a big upswing. The rare coin market has already been red-hot, along with many other collectibles in 2021. Blame it on the pandemic, when Americans were stuck at home. Millennials and others began sifting through family coin collections handed down from their grandparents, took an interest in collectibles and the rare coin market has benefited.

In June 2021, the Rare Coin Values Index hit a new all-time record high of 434.28. (The Rare Coin Value Index is based on the combined percent change in retail prices for 87 rare United States coins and is updated monthly.)

The last time Wall Street got involved in rare coin investments in a major way was in the late 1980’s – after third party grading and certification legitimized numismatics as an asset class. Back then, Kidder, Peabody & Co. launched the American Rare Coin Fund. Merrill Lynch opened the NFA World Coin Fund Limited Partnership. UBS developed a rare coin division to advise its high net worth clients on numismatics. And, the price of rare coins exploded higher.

Today, interest in portfolio diversification with tangible assets like rare coins is indeed growing – otherwise firms like Blackstone wouldn’t be jumping into a half a billion dollar deal like this. Yes, we take this as a sign that the numismatic investor base can grow.

What lies ahead for rare coins now?

“There have been a few multi-million blockbuster sales in 2021 for great rarities…Some experts believe it is only a matter of time before prices start moving noticeably higher for rare coins pursued by the average collector,” U.S. Coin Values said.

This Blackstone deal is just another sign that the rare coin market is entering a new phase – attracting new investors and creating more interest and demand, which will be a positive price force going forward.

“I think an acquisition by one of the world’s largest investment firms says a lot about the excitement around the fast-growing collectibles industry,” Certified Collectibles Group president Max Spiegel said. “There are a lot of highly experienced and successful investors getting into this space, which reflects not only the size of the collectibles market today, but also its growth potential.”

Last but not least: A note about Blanchard

You may already know this, but Blanchard has a long-term connection with NGC and coin grading.

Blanchard proudly offers coins handpicked by John Albanese, who is the top numismatist and coin grader working in the rare coin market today. Albanese is America’s leading professional numismatist and he is a world-renowned authority on coin grading and the rare coin market. He co-founded Professional Coin Grading Service (PCGS) before launching Numismatic Guaranty Corporation (NGC), where he personally graded more than one million coins.

If you’d like more insights on what this could mean for your rare coin investments, or if you are interested in adding to your portfolio, please contact a Blanchard portfolio manager at 800-880-4653.

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.

The Gold – U.S. Dollar Connection

Posted on — Leave a commentInvesting in gold may have felt like a roller coaster ride this year.

Gold began 2021 just above the $1,900 an ounce level. Then, gold retreated to around $1,680 in late March. By late May, gold prices surged back above $1,900 an ounce. Recently, gold dipped to about $1,800 an ounce.

The price of gold is influenced by many factors. Key drivers of gold include interest rates, inflation, the amount of U.S. dollars in circulation (money supply), U.S. debt levels, political and economic stability and many other factors including the level of the U.S. dollar.

Today, we’ll focus in on a recent influence that has pressured gold lower lately – the U.S. dollar.

Economists like to call the connection between the U.S. dollar and gold – an inverse correlation. In simple terms, that means when the U.S. dollar climbs – gold tends to fall and the opposite is true as well. When the U.S. dollar falls, gold tends to increase in price.

As of early July, the U.S. Dollar index is 3% higher on the year, while gold is about 5% lower on the year.

The surprise strength in the U.S. dollar has weighed on gold in recent weeks.

Looking back 20 years – what’s the long-term dollar trend?

Let’s look at current levels in historical context. In June 2001, or 20 years ago, the U.S. dollar index stood at nearly 119.00.

Today? The U.S. dollar index stands at 91.46.

The long-term trend of the U.S. dollar is down. There are many reasons for this – including the gigantic amount of U.S. government debt – which now stands at a historic all-time high at $28.4 trillion.

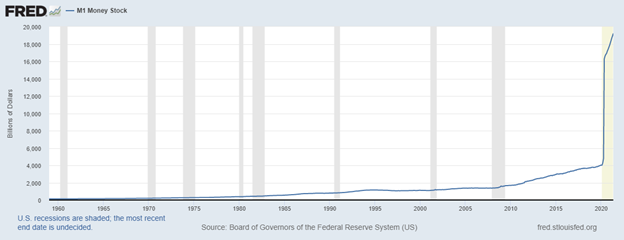

Another reason for the downtrend in the U.S. dollar? The Federal Reserve keeps expanding the money supply – or printing more dollars for circulation. Take a look at this chart from the St. Louis Federal Reserve (FRED). The amount of M1 money stock has literally gone straight up in recent years.

The long-term downtrend in the U.S. dollar is an important positive factor for gold investors in the years ahead, and is one of the key drivers that is expected to push gold to new all-time highs.

As the Federal Reserve continues to devalue our dollar by printing more, and the U.S. government continues to put our credit at risk by taking on more debt – gold will continue to increase in value.

What does all this mean for gold ahead?

The Wells Fargo Investment Institute published a new investment strategy report on July 6. Here’s what they said.

“Gold has had a rough 2021 because the U.S. dollar has surprisingly rallied.”

What else did they say?

“We think gold represents good value at today’s levels. Investor sentiment appears overly negative and we are expecting the U.S. dollar to fade and real interest rates to remain low through 2021.”

By year-end, the Wells Fargo Investment Institute targets gold in the $2,000-$2,100 range.

That represents a 16% increase from gold’s level today.

The long-term drivers to push the U.S. dollar lower remain in place. The U.S. debt and the massive dollar money supply aren’t going away anytime soon.

That means today’s gold market offers you, the long-term investor, a tremendous opportunity. Do you own enough?

Want to read more? Subscribe to the Blanchard Newsletter and get our tales from the vault, our favorite stories from around the world and the latest tangible assets news delivered to your inbox weekly.